Summarizing the long article below, the author emphasizes that after many decades of doing work with stocks and valuations, he continues to be convinced that "Earnings Determine Market Value," or EDMV.

Now, the other "face," the pathological liar face, is "Emotions Determine Market Value." You see where this is headed. The stock market has long been a balance between fear and greed, bulls and bears, emotion and earnings. I won't change. You need to be aware of the forces and act accordingly.

What does this have to do with buying a business? You can invest in the stock market and let external forces determine some of the results. Or, you can couple your money with your efforts and multiply the results. The folks I work with are tired of others making money off their efforts and want to use that for their own benefit. Along the way, you get a whale of a lot of self-satisfaction.

Still, when buying a business, remember that the EDMV principle works here as well. You must have earnings, and the value of the assets is only a small part of the equation. In the extreme, an insurance agent has few assets--a desk, phone, transportation. The earnings are from his/her energy.

Sometimes assets are a liability. For instance, I currently have a client who sees how much the company has spent on accumulation of assets and believes the business should be worth what those cost over decades. That is NOT going to happen. The earnings produced by those assets create the value.

GROWTH

Just as with common stocks, growth influences price. If EDMV, then the future value of those earnings is factored in. For example, in the examples below, some stocks are priced at 11 times earnings (P/E Ratio) and some are valued at 25 times. The difference? The current assessment of the market as to the growth and sustainability of that growth. Plus some emotion!

YOUR BUSINESS

Your business or the one you will buy is valued similarly. But at a much lower P/E Ratio, and the "Earnings" need to be adjusted to factor out the legal and sometimes semi-legal things that business owners may do to reduce their tax burden.

Successful businesses pay a lot of taxes, but Supreme Court Justice Learned Hand ruled long ago that none of us are obligated to pay more than our legal share. Sometimes, the rules are shaded to be more than was intended, and that is where I come in to adjust those earnings.

At the end of the day, you must know how much the business earns that is then available to pay you and the "bank."

NET OWNER BENEFIT (NOB)

Small businesses generally sell for multiples of one to four times NOB. Growth is a factor, size is a factor, but you must earn a salary and the "bank" should be paid whether the bank is an actual financial institution, your retirement plan or your savings account.

BACK TO EDMV

This gentleman has a valid point. When buying a business, practice this as well.

Stocks Are Two-Faced, And One Is A Pathological Liar

Summary

- Both common sense and logic would dictate that future investment success and results are dependent upon possessing an accurate understanding of the most relevant factors that drive future stock movements.

- In the long run - Earnings Determine Market Price.

- In the short run - Emotions Determine Market Price.

Introduction

I believe that it

behooves all investors that invest in common stocks to have a coherent

understanding of what I consider the most important principle regarding

investing in stocks. Moreover, a cogent awareness of this principle

relates to having a relevant and valid answer to the following important

question: What drives the future price of a common stock?Both common sense and logic would dictate that future investment success and results are dependent upon possessing an accurate understanding of the most relevant factors that drive future stock movements and their direction - in the long run. Otherwise, how could an investor ever determine whether investing in a given company (common stock) makes sense, or if it represents an attractive investment opportunity?

Therefore, I offer this article as a dissertation on the primary factor that drives the future stock prices of a publicly traded common stock. Moreover, this same factor is the driver that creates the value of all businesses, public or private. In other words, with this article I am endeavoring to illuminate the primary principle that generates current and future value to business owners.

Admittedly, most of what I will be discussing I consider as "stating the obvious." However, as it is with many investing principles and financial jargon, the obvious is often overlooked or missed. More plainly stated, over my long career in the financial services industry, I have observed a penchant for making simple concepts complicated. In Western Pennsylvania, where I grew up, this was commonly referred to as "complicating a one-car funeral."

"It's the Earnings, Stupid"

With

the above in mind, I respectfully ask the reader to allow me to state

the obvious. It is simply the earnings power of any business that gives

it value, past, present and future. The more earnings power a business

possesses, the more value it is capable of delivering to its owners.

Once again, this simple and obvious truth applies to every business,

public or private. Consequently, if this is truth, and I contend that it

is, then doesn't it make sense for investors in, and owners of,

businesses to focus on earnings, first and foremost?Frankly, I believe it does make sense for an owner of a business to focus primarily on the company's earnings power. However, my extensive experience in the investing industry suggests that most investors focus too much on price movements over profits. I believe this is a mistake, and yes, I believe it is an obvious mistake that can, and should, be avoided.

The 2 Faces of a Stock's (Business) Performance

I

have long used the simple acronym - EDMP - to keep me focused on this

important principle regarding the primary driver of a common stock's

price. So much so, that I named the money management firm I co-founded

based on it. The acronym EDMP stands for Earnings Determine Market Price

(in the long run).Fortunately for me, this principle was burned into my brain by my Economics professor in college. My professor's name was Alvin F. Terry, and every day, he started the investment course he taught in the following manner. Once we are all settled in our seats, Prof. Terry would walk up to his desk and literally and vigorously pound the table with his fists while shouting - EARNINGS DETERMINE MARKET PRICE! Every day, without fail, class was started with this fanatic ritual.

Needless to say, thanks to my passionate and enthusiastic professor, the obvious long-term driver of a common stock's price became forever imprinted into my psyche. In fact, his antics made such an impression upon my young mind, that it became the focal point of my life's work. My entire career, that now spans more than four decades, has been dedicated to validating Prof. Terry's thesis. Moreover, I am happy to report that my research and experience has proven to me that his simple and obvious hypothesis was both valid and true. Soon, I will present evidence supporting the truth behind my professor's words.

However, before I do that, I believe it's important to present and discuss a complicating factor that causes many investors to overlook the obvious. My research also uncovered that there is an evil twin sister - EDMP - that applies to the shorter run. Emotions Determine Market Price, in the short run, and it is this fact that creates the primary reason why investors often lose their focus and miss the obvious.

As human beings, we are emotional creatures, and when our emotions are in a heightened state, critical thinking goes out the window. This applies to all aspects of life, and certainly applies to how we handle or invest in our stock portfolios. In other words, in the short run, it is easy to become blinded by the two most powerful emotions that investors are often forced to deal with - fear and greed. Of the two, I believe that fear is both the most dangerous and most powerful emotion that investors must deal with. Fear is associated with anxiety, and when we are frightened, we are most likely to cast reason aside.

What this all boils down to is the reality that there are two faces of performance. To me, the true and most important performance face of a business is its operating performance. This is most commonly evaluated based on a company's bottom line, i.e. its earnings. Consequently, since I'm a long-term investor, I have also trained myself to pay more attention to the business behind the stocks I own, and less attention to the daily gyrations of their short-term stock prices in an auction marketplace.

Unfortunately, this is apparently difficult, or as I stated earlier, overlooked by many, if not most, investors. Instead of trusting their company's bottom line, they instead either obsess or worry about their investment based on whether the price of their stock is going up or down. And as I stated many times before, if the price of a company's stock is falling, it's a bad stock. In contrast, if the price of a stock they own is rising, it's a good stock. But most pertinent is the actuality that these judgments are often made with no informed regard to the fiscal health and strength of the underlying businesses they own.

The problem with this kind of emotional behavior is that all too often it motivates people to buy a stock they should be selling, and sell a stock they should be buying. A great company's stock price falls, and instead of recognizing it as the opportunity it is, they panic and sell. This often results in selling a valuable asset for significantly less than it is truly worth. This behavior caused more people to lose money during the Great Recession, than the Great Recession itself. Personally, I believe it's virtually always a bad idea to sell a valuable asset for less than its intrinsic value just because you are scared by the temporary actions or behaviors of others.

Real-world Examples of the Importance of Earnings

As

I previously mentioned, my finance professor's passionate teachings

inspired me to dedicate my life to evaluating his common sense thesis.

However, with the investment world almost universally focused on stock

price movements, I was frustrated at almost every turn as I looked for

evidence to support the logical notion that earnings determine market

price. Therefore, I took matters into my own hands and developed

F.A.S.T. Graphs™, the earnings and price-correlated, fundamentals-based

stock research tool.Once armed with my creation, I was empowered to examine the long-term earnings and price correlation, and I now contend functional relationship on thousands of companies over many decades. The evidence supporting the importance of earnings is both overwhelming and incontrovertible. No matter whether earnings go, up, down or sideways, on graph after graph, earnings and price will move in tandem. Moreover, if the stock price strays away from its earnings-justified valuation (over or under), inevitably it will come back into alignment with earnings. Therefore, not only is this a common sense hypothesis, it is supported by a preponderance of undeniable real-world evidence.

Since a picture is worth a thousand words, I will offer the following examples via the F.A.S.T. Graphs™ research tool to illustrate the veracity of what I have thus far written. Importantly, the reader should note that the focus of the following exercise is on the long-term relationship between earnings and stock price. Consequently, even though some of the following examples do pay dividends, they will be excluded from the following presentation. More clearly stated, this is not a total return exercise, instead it is an exercise to illustrate that in the long run, earnings drive stock prices and trump price volatility.

(Note: In all

examples, where possible, I will present my maximum 20-calendar year

graphs. On any graph over 15 calendar years, only every other year's

data is typed onto the graph, but all data is plotted.)

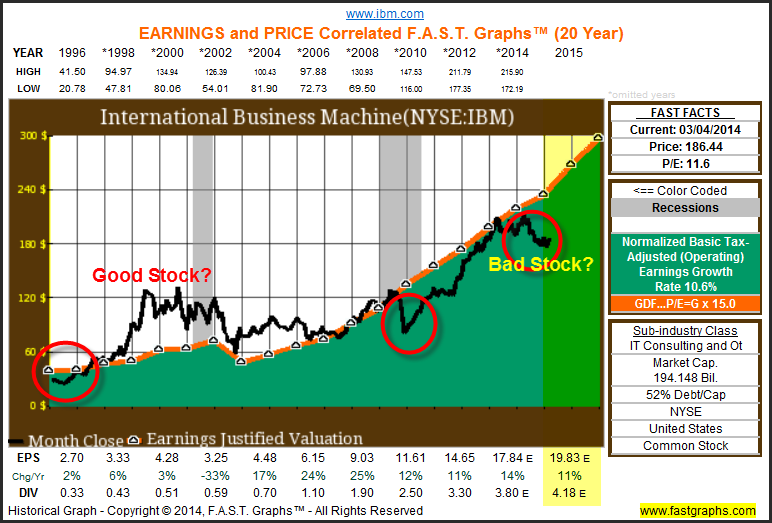

International Business Machines (IBM)

International

Business Machines Corporation provides integrated solutions, such as

consulting, delivery, and implementation services; enterprise software;

systems; and financing for clients.I chose IBM as my first illustration, because I feel it represents a quintessential example, or poster child for the good stock when prices are rising and bad stock when prices are falling notion. With the first IBM graph, I plot earnings per share since 1996, to include estimates for 2014 and 2015.

Clearly, IBM has been an earnings powerhouse over that time frame, with the only exception being 2002. To reiterate and focus on my thesis, the first face of IBM's performance, earnings, present a true picture of this company's valuation. Earnings have grown at an average annual compound rate of 10.6%.

(click to enlarge)

Interestingly, IBM has recently been a much-maligned company, as evidenced by many recent articles published here on Seeking Alpha. Simply search with its ticker symbol, and you will find many recent examples of negative articles on this blue-chip technology company. Therefore, we see evidence supporting IBM as a bad stock based on its poor stock price performance over the last two years or so. Ergo, price-wise, IBM bad stock, bad stock.

In contrast, this is in spite of the fact that the company's earnings have remained solidly in an uptrend, and are expected to continue advancing over the next several years by the consensus of analysts following the company (yellow highlights). However, a quick review of the earnings and price-correlated graph below illustrates that IBM's stock price has followed earnings over the long run.

Moreover, we see clear evidence that the best time to purchase IBM was during those times when its stock price fell below its earnings-justified level. In other words, when many investors thought it was a bad stock because its stock price was down. We see that in the beginning of 1996, again at the end of 2008 (The Great Recession), and once again today. These are times when the evil twin sister, EDMP (Emotions Determine Market Price-in the short run) dominates investors' minds. On the other hand, we simultaneously see evidence supporting the true performance generator, EDMP (Earnings Determine Market Price-in the long run).

(click to enlarge)

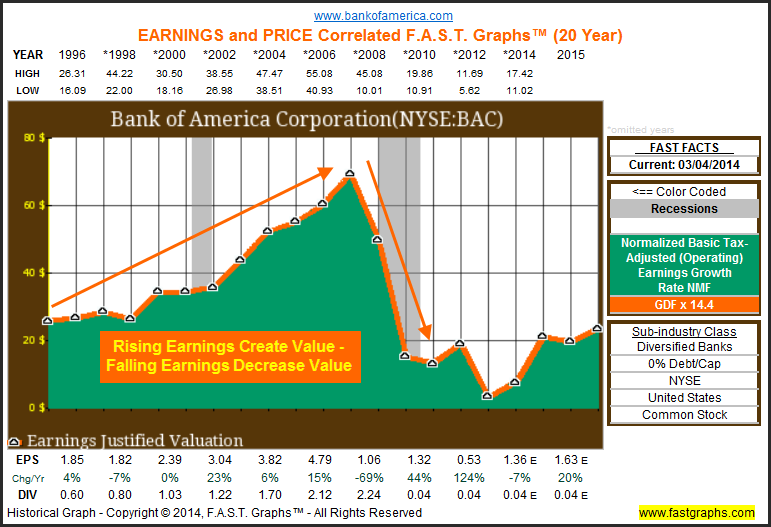

Bank of America (BAC)

Bank

of America Corporation, a financial institution, offers a range of

banking, investing, asset management, and other financial and risk

management products and services to individual consumers, small- and

middle-market businesses, institutional investors, large corporations,

and governments.With my second example, I review the earnings history of Bank of America. I chose this example because it provides clear evidence not only of the importance of earnings, but also to the idea that where earnings go, stock price is sure to follow. With the first Bank of America graph, we see strong earnings growth for the first 11 years, followed by a collapse of earnings and somewhat erratic results thereafter.

(click to enlarge)

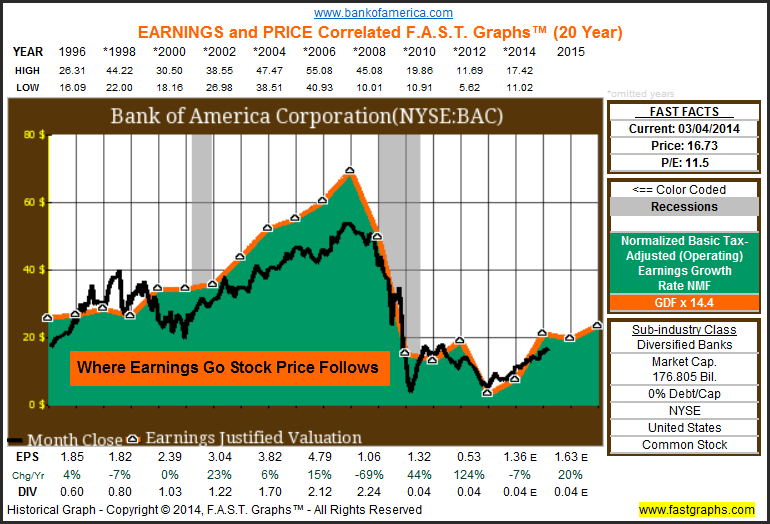

Consequently, when you overlay monthly closing stock prices to the earnings graph, the importance of earnings as a driver of stock price is clearly evident and undeniable. Where earnings went, stock price followed in the long run, up, down, and sideways.

(click to enlarge)

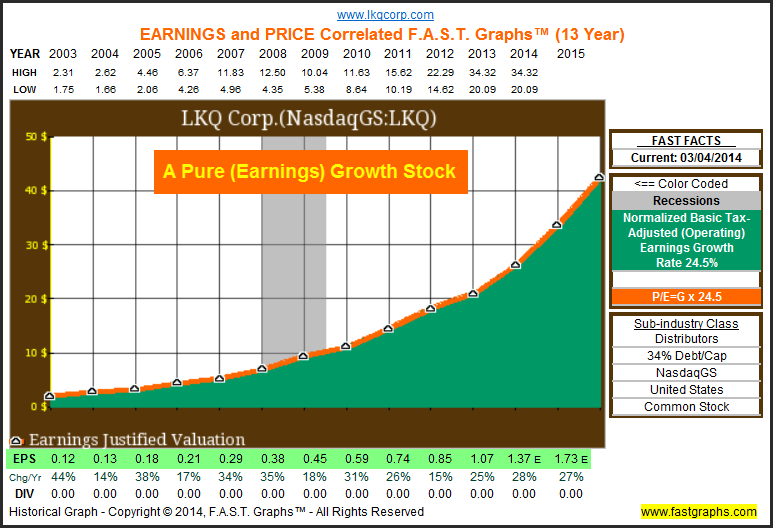

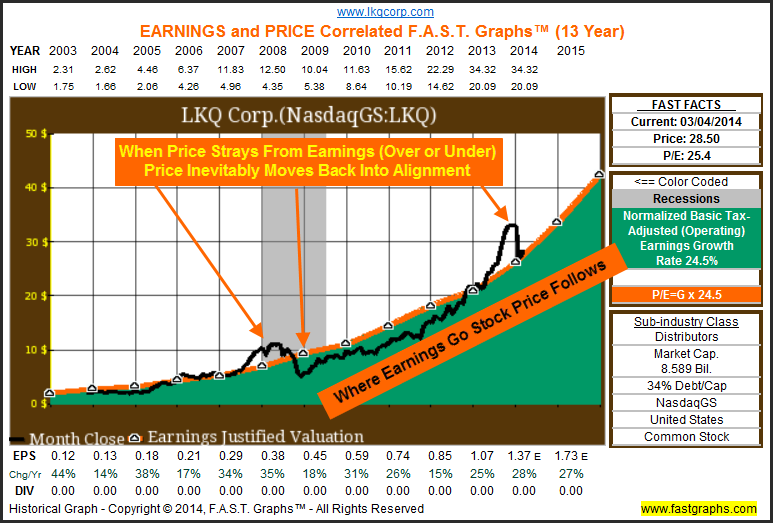

LKQ Corp. (LKQ)

LKQ

Corporation provides replacement parts, components, and systems needed

to repair cars and trucks. The company has operations in the United

Kingdom, Canada, Mexico, and Central America.With my final example, I present LKQ Corp. as a quintessential example of a pure growth stock. Unlike my previous two examples, this company does not pay, and never has paid, a dividend. Therefore, the sole source of return that owners (shareholders) of this rapidly-growing business receive, or currently can expect to receive, is based purely on the company's earnings power.

I also chose this example because it has only been publicly traded since October 2003. Therefore, by looking at the horizontal EPS (earnings per share) column at the bottom of the graph, each year's earnings per share is both plotted and typed on to the graph. The earnings power of this company has been both exceptional and consistent, averaging 24.5% per annum since going public.

(click to enlarge)

When we overlay monthly closing stock prices to LKQ's earnings, we discover as pure a long-term correlation between earnings and price as you will ever see. Moreover, we see evidence that when the company's stock price rose above earnings (the orange line), as it did in 2007 and 2008, that price soon came back to earnings. Once again, we see evidence supporting the idea that it's more important to focus on a company's earnings power over the long run than it is to focus on short-run price volatility.

The earnings power of a business is tangible and reasonably predictable. The investor can review important fundamentals, such as the balance sheet, profit margins, sales growth, etc., and derive a reasonable evaluation of the strength and health of the business behind the stock. In contrast, stock price volatility is ephemeral and often a pathological liar. In other words, price cannot always be trusted.

(click to enlarge)

The Moral to the Story

Serendipitously, Warren Buffett published his 2013 Letters to Berkshire Shareholders

as I was preparing this article. What follows are a few excerpts of his

letter that speak directly to the importance of focusing on long-term

business results over short-run stock price volatility. These excerpts

are based on the section of Warren's letter titled: Some Thoughts About Investing. Appropriately, he starts this section off with a quote by Benjamin Graham from his book The Intelligent Investor, as follows:"Investment is most intelligent when it is most businesslike."In order to illustrate the importance of thinking like a business owner, Warren utilized examples of two small non-stock investments he made in mid-1986 and 1993. One was a farm 50 miles north of Omaha, Nebraska that he purchased in 1986, and the other was a New York rental property adjacent to NYU that he made in 1993. He used these as focal points on why he believes that investors in common stocks should ignore price volatility. My first excerpt is as follows:

"With my two small investments, I thought only of what the properties would produce and cared not at all about their daily valuations. Games are won by players who focus on the playing field - not by those whose eyes are glued to the scoreboard. If you can enjoy Saturdays and Sundays without looking at stock prices, give it a try on weekdays."Then, Warren Buffett goes on to say:

"There is one major difference between my two small investments and an investment in stocks. Stocks provide you minute-to-minute valuations for your holdings whereas I have yet to see a quotation for either my farm or the New York real estate."Then, he goes on to put it all in perspective with the following rather extensive excerpt:

"It should be an enormous advantage for investors in stocks to have those wildly fluctuating valuations placed on their holdings - and for some investors, it is. After all, if a moody fellow with a farm bordering my property yelled out a price every day to me at which he would either buy my farm or sell me his - and those prices varied widely over short periods of time depending on his mental state - how in the world could I be other than benefited by his erratic behavior? If his daily shout-out was ridiculously low, and I had some spare cash, I would buy his farm. If the number he yelled was absurdly high, I could either sell to him or just go on farming. Owners of stocks, however, too often let the capricious and often irrational behavior of their fellow owners cause them to behave irrationally as well. Because there is so much chatter about markets, the economy, interest rates, price behavior of stocks, etc., some investors believe it is important to listen to pundits - and, worse yet, important to consider acting upon their comments.Clearly, legendary investor Warren Buffett and his partner Charlie Munger understand the importance of focusing on the intrinsic value of the assets you invest in, while simultaneously eschewing short-term price volatility.

Those people who can sit quietly for decades when they own a farm or apartment house too often become frenetic when they are exposed to a stream of stock quotations and accompanying commentators delivering an implied message of "Don't just sit there, do something." For these investors, liquidity is transformed from the unqualified benefit it should be to a curse.

A "flash crash" or some other extreme market fluctuation can't hurt an investor any more than an erratic and mouthy neighbor can hurt my farm investment. Indeed, tumbling markets can be helpful to the true investor if he has cash available when prices get far out of line with values. A climate of fear is your friend when investing; a euphoric world is your enemy."

Summary and Conclusions

The

performance of common stocks truly is two-faced. One face, the

important one, represents the face of reason and focuses on the true

driver of economic value to investors. The second face, is quite often a

pathological liar, and for the most part, full of heightened emotion

and simultaneously often devoid of logic. Yet somehow, and inexplicably

to me, most investors are prone to trust the liar more than they do the

face of truth and reason.Judging your common stock investments based solely on whether the price has recently risen or fallen is madness. As Warren Buffett has tried to teach us for many years, it is wiser to invest in businesses than it is trying to time or play the market. These principles are especially important and relevant to those retired investors who are dependent upon the performance of their portfolios to support their livelihoods. Our futures and the futures of our families are simply too important to trust to hysteria and lies.

In conclusion, what I've written about in this article was solely focused on what drives the long-term stock prices of common stocks. Price action is only one component of total return, the other is dividend income. However, just as earnings drive long-term stock price performance, they are also the source of dividend income. Therefore, focusing on the earnings power of any publicly traded business you choose to invest in just seems like common sense action to me.